The above information is recorded in the real estate market report in April published by DKRA Group recently. Accordingly, for the resort villa segment, supply continued to decrease from the end of the second quarter of 2022, the number of projects launched on the market was extremely modest, supply decreased by 69% compared to the previous month and decreased by 98% compared to the same period.

Specifically, in the month, there were only 2 projects, 1 new project and 1 project opening for sale in the next phase, with 12 units joining the supply. The North and the South continued to lead the supply of the whole market, while the Central region recorded no new projects for 4 consecutive months.

Meanwhile, the consumption volume is only 3 units, equivalent to a consumption rate of 38%. This comes from very low demand, new projects have slow sales. 60% of primary projects have closed their baskets without recording any transactions.

According to DKRA, the primary selling price level has not changed compared to last month. In the North, the highest primary selling price was recorded at 28.8 billion VND/unit and the lowest was 8.5 billion VND/unit.

In the South, the highest primary price is 52.2 billion VND/unit and the lowest is 29.1 billion VND/unit. It is expected that in the next month, market supply and demand may increase slightly but without many clear fluctuations, mainly concentrated in Phu Quoc. Interest rate support policies, principal grace period, etc. are still applied by many investors to support buyers in this segment.

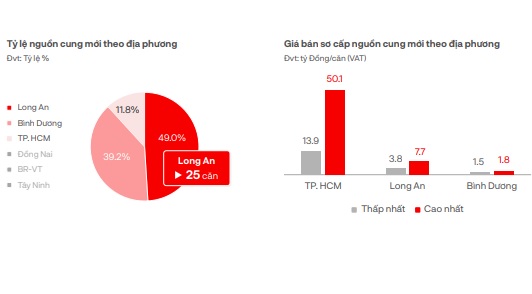

Primary supply and selling prices by location.

In the resort townhouse/shophouse segment, in April, there were only 20 units added to the supply from 2 new projects, an increase of 33% compared to the previous month but still at a very low level, mainly concentrated in Phu Quoc and Tuyen Quang . Meanwhile, the consumption volume was only 8 units, a decrease of 99% compared to the same period last year.

Market demand is still modest, only equivalent to 1% compared to the same period in 2022. New projects all have slow sales, especially primary projects, more than 60% of projects have closed their baskets without recording transactions. Primary selling prices have not fluctuated compared to the previous month, and discount policies of 30% - 40% of selling prices for quick payment continue to be applied to stimulate market demand.

It is expected that in the coming month, market supply and demand will increase slightly, focusing on projects with complete legal documents and developed by investors with strong financial potential. Meanwhile, the North and the South are still the leading regions in supply, while the Central region continues to maintain a scarcity of new projects.

In the Condotel segment, 84 units were added to the new supply from 2 projects, 1 new project and 1 project in the next phase, down more than 58% compared to March and down 17% compared to the same period. New consumption reached 32 units, equivalent to a consumption rate of 38%.

Condotel consumption remains low.

Supply is still assessed to be at a very low level, down more than 58% compared to the previous month and down approximately 17% compared to the same period. The North and Central regions are still the leading regions in terms of supply. The South, in particular, has continued to record no new supply for 4 consecutive months.

Primary selling prices have not fluctuated much, preferential programs, quick payment discounts, principal grace periods, interest rate support, etc. are still widely applied to attract customers' attention. Projects with full legal documents, operated by 4* - 5* international brands are still prioritized by the market and have a more positive sales situation compared to the general market level.

In the North, the lowest primary price is 31 million VND/m2, the highest is 56.1 million VND/m2. Despite the gloomy market, the selling price in the South is very high with the lowest primary price being 109.6 million VND/m2, the highest reaching 139.4 million VND/m2.

It is expected that in the coming month, market supply and demand will continue to recover thanks to positive information from the Government , however there will not be many breakthroughs in the short term.

Source

![[Photo] Binh Trieu 1 Bridge has been completed, raised by 1.1m, and will open to traffic at the end of November.](https://vphoto.vietnam.vn/thumb/1200x675/vietnam/resource/IMAGE/2025/10/2/a6549e2a3b5848a1ba76a1ded6141fae)

Comment (0)